Most franchise stores do not need more products on the menu. They need a tighter mix: VSC as the anchor, GAP as the second volume line, a few ancillaries buyers actually keep, and one non-cancellable theft-tech product that protects retained gross. That is where the real lift sits.

Late-2025 store economics made that menu discipline a lot more urgent. New-vehicle front-end gross fell to $279, while average F&I profit per retailed unit reached $1,995 in Q4 2025 and hit a record $2,025 in November. Public groups pushed even higher, averaging $2,534 in Q3 2025. At the same time, dealer sentiment stayed cautious, with only 45% of surveyed rooftops expecting F&I to improve 2025 profitability. That gap explains the real pressure point in today’s F&I office: booked gross matters on the delivery report, but retained gross decides what the store actually keeps after cancellations and chargebacks clear.

That tension shows up when a store posts a strong month in the box, then gives part of it back through refunds tied to products customers never fully valued.

The safest default mix still starts with a vehicle service contract and GAP. Late-2025 benchmarks reported by F&I and Showroom put VSC penetration at 46%, GAP at 40%, paint and fabric at 20%, prepaid maintenance at 17%, and tire-and-wheel at 10%. That is a balanced menu, not a wide one.

Two things matter in that spread. First, VSC and GAP still do the heavy volume work. Second, the ancillary layer is not filler. Those lines generated roughly one-third of 2025 F&I income, which means the mix gets safer when income comes from more than two refund-exposed products.

The last slot should do a different job than the first five. A non-cancellable theft-tech product does not replace core protection. It hardens retained gross after funding, especially in stores where refinance activity and early payoffs keep eating back-end income months later.

The back end is doing the heavy lifting now. Haig Partners reported that public dealership groups averaged $2,534 in F&I gross profit per vehicle in Q3 2025, up 5.2% year over year, while retail benchmarks showed new-vehicle front-end gross down to $279 late in the year.

At the store level, Q4 2025 F&I PVR averaged $1,995 and touched $2,025 in November. When the front end is that thin, every lost dollar in the box hits operating income fast. That changes how a dealer principal should judge F&I products. The issue is not whether a line can sell once. The issue is whether the product holds gross through payoff, refinance, and post-sale scrutiny.

For the GM and F&I director, the implication is practical. A menu heavy on cancellable products can print a good month and still disappoint by quarter close. A weak ancillary mix leaves fewer ways to grow PVR without forcing the same two products harder. The better play is a menu built around high-penetration core lines, stronger use-case selling, and one fully earned technology product that gives the store gross it can count on.

F&I products are no longer a nice extra on the deal. In many stores, they are the difference between an acceptable deal and a skinny one. That is why retained PVR deserves boardroom attention, not just end-of-month attention.

Customer acceptance is strongest when the buyer can picture the bill or the inconvenience. In its 2023 industry report, Protective Asset Protection found that dealers most often cited expensive electrical components at 49%, advanced vehicle technology at 46%, and emergency roadside needs at 45% as purchase drivers.

That is how VSC should be sold right now. Skip the broad warranty talk. Show the shopper the expensive equipment living behind today’s screen-rich, sensor-heavy vehicle: cameras, control modules, infotainment hardware, and driver-assist electronics. The presentation lands when the customer can connect the product to something on the vehicle they already use every day.

The same rule holds for ancillary lines. Tire-and-wheel works when the road-hazard claim is easy to picture. Prepaid maintenance works when service pricing is concrete and interval-based. Appearance protection works when the dealership explains what the plan covers, how the remedy is handled, and where the customer returns for help.

Connected-car theft products should be presented the same way. Start with visible utility, then move to the payout. A buyer responds better when they first see vehicle location, alert functions, and recovery support, then hear about the financial backstop. Concrete claim scenarios beat generic “peace of mind” language every time.

Booked PVR and kept PVR are different numbers, and too many stores still manage from the first one. Coverage from Auto Finance News, citing Kerrigan Advisors, found that only 45% of 635 dealerships expected F&I to improve 2025 profitability, while 7% expected a negative profitability impact.

That concern makes sense when chargebacks are treated as what they are, delayed gross reversals. The trigger might be an early payoff. It might be a refinance six months later. It might be buyer remorse after a rushed explanation, or a relative, lender, or outside adviser telling the customer the product was unnecessary.

In some portfolios, AFSA-cited data shows more than 25% of F&I product revenue can end up canceled and refunded. A month with strong sales on paper can still look weak by the time those reversals hit accounting. That is why retained PVR needs a standing place in every operating review, right beside penetration and product count.

Once a store sees the gap between sold gross and kept gross, the menu decision gets clearer. Products with no pro-rata refund liability do more than add revenue. They change the stability of the whole back end, because the store is no longer waiting to see how much of that month’s profit survives the next quarter.

Lower cancellation rates usually start with timing, not with a new closing line. As CBT News reported, more than 60% of buyers are comfortable starting the purchase process online, and a follow-up around two weeks after delivery can reduce cancellation risk. The strongest stores let education start before the customer ever sits in the finance office.

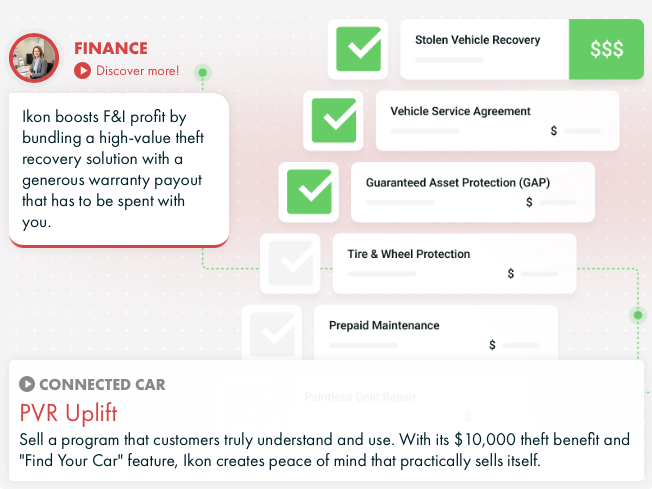

Ikon belongs in the mix as a stabilizer, not as a replacement for your core protection lines. In its look at non-cancellable technology, Ikon Technologies positions a connected-car product with a $10,000 theft benefit as a fully earned sale that is not exposed to pro-rata cancellation.

That matters most in rooftops where VSC and GAP volume is healthy, but lower-acceptance ancillaries keep bleeding gross after the fact. In that setting, Ikon works as the sixth menu slot or as the line that replaces a weak appearance or maintenance offer. The store gets gross that stays booked. The buyer gets something they can understand in a few minutes.

The value story is concrete because the technology is visible. With Ikon Connect, the customer can use connected-car tools such as vehicle location, alerts, and direct dealership contact inside the app, while the theft recovery benefit provides a specific $10,000 backstop if the vehicle is stolen and not recovered. That is easier to explain than a vague promise tied to an event the customer may never picture.

For dealers, the appeal is simple. Ikon hardens retained PVR without asking the menu to give up VSC or GAP volume. It fills the fragile spot in many menus, the slot that should contribute back-end gross without setting up a later clawback.

The strongest mix in this market is narrower and smarter, because front-end gross around $279 leaves no room for products that look good on the delivery log but wash out later. VSC and GAP still anchor the menu. Ancillary lines still matter because they already contribute about one-third of current F&I income. The missing piece in many stores is the slot that protects kept gross, not just sold gross.

Digital timing belongs in the same conversation. When buyers see F&I products earlier, hear the same examples in the store, and get a follow-up after delivery, they keep more of what they buy. November 2025’s $2,025 PVR record only matters if the store can hold onto it. That is the operating difference between a strong month and a durable one.

Run a 90-day mix audit with the dealer principal, GM, and F&I director. Measure booked PVR against retained PVR, track penetration and cancellation by product, review digital presentation timing, and check day-14 follow-up completion. Then make one hard menu decision: keep, cut, or replace the weakest ancillary slot, using Ikon’s non-cancellable $10,000-benefit position as the comparison point.

A strong franchise-store target is usually about 1.5 to 2 or more F&I products per deal. The safer build is one backbone item, usually VSC or GAP, plus one ancillary or non-cancellable add-on. The scorecard is retained PVR, because a loaded menu means little if later cancellations strip it back.

Customers usually cancel after signing because the price felt heavy, the benefit never landed clearly, or someone outside the store told them to unwind it. In some portfolios, more than 25% of sold F&I product revenue gets canceled and refunded. Early digital explanation plus a follow-up around two weeks after delivery cuts that regret cycle.

F&I products should appear during the online shopping phase, not for the first time inside the finance office. More than 60% of buyers are comfortable starting the purchase process online, and 68.5% of dealers already say they are likely to let shoppers research options there. Earlier visibility gives the in-store menu a much cleaner handoff.

The best customer acceptance sits around products tied to expensive electronics, advanced vehicle tech, and roadside help. Dealer-reported motivations came in at 49% for electrical components, 46% for advanced vehicle technology, and 45% for emergency roadside needs. Volume leaders still remain VSC at 46% penetration and GAP at 40%, because the value story is easy to connect to real ownership cost.

No, a non-cancellable product should complement GAP or a service contract, not replace them. VSC and GAP still anchor the menu at 46% and 40% penetration, and they remain the biggest back-end volume drivers in most franchise stores. The non-cancellable line works best as retained-gross protection layered onto that core mix.

Ikon stands out when a store already sells solid VSC and GAP volume but struggles to keep profit on weaker ancillary products. The dealer case is straightforward: a non-cancellable sale with no pro-rata refund exposure. The buyer case is just as clear, because connected-car technology is paired with a specific $10,000 theft benefit that is easy to understand and easy to value.

.jpg)

.jpg)